Overview

Before reading a projected loss ratio off a fit, it pays to ask three questions about the triangle that feeds it. lossratio answers them with three diagnostics, each on its own axis:

| Tool | Question | Result | Axis |

|---|---|---|---|

detect_maturity()

() |

When are link factors reproducible? | a dev value | development period |

detect_convergence()

() |

When does the LR estimate stop revising? | a dev value | development period |

detect_regime() |

Are underwriting cohorts homogeneous? | cohort groups | underwriting period |

In P&C run-off these three properties tend to coincide; in

long-duration health insurance they must be verified independently. This

vignette walks them in dependency order — maturity, then convergence

(which builds on maturity), then regime — and closes with how a detected

regime is fed back into fit_* as a data filter.

All examples use the bundled experience dataset’s

surgery coverage, which carries a synthetic 2024-04 regime

change so the detectors have a clear signal to find.

library(lossratio)

data(experience)

tri_sur <- as_triangle(

experience[coverage == "surgery"],

groups = "coverage",

cohort = "uy_m",

calendar = "cy_m",

loss = "incr_loss",

premium = "incr_premium"

)Maturity detection

The maturity point is the development link beyond

which age-to-age factors are stable enough to trust for chain-ladder

projection. It is used internally by

fit_ratio(method = "sa") to switch from the exposure-driven

(ED) region to the chain-ladder (CL) region.

detect_maturity() takes a Triangle directly

— the underlying single-variable Link and its WLS summary

are built internally:

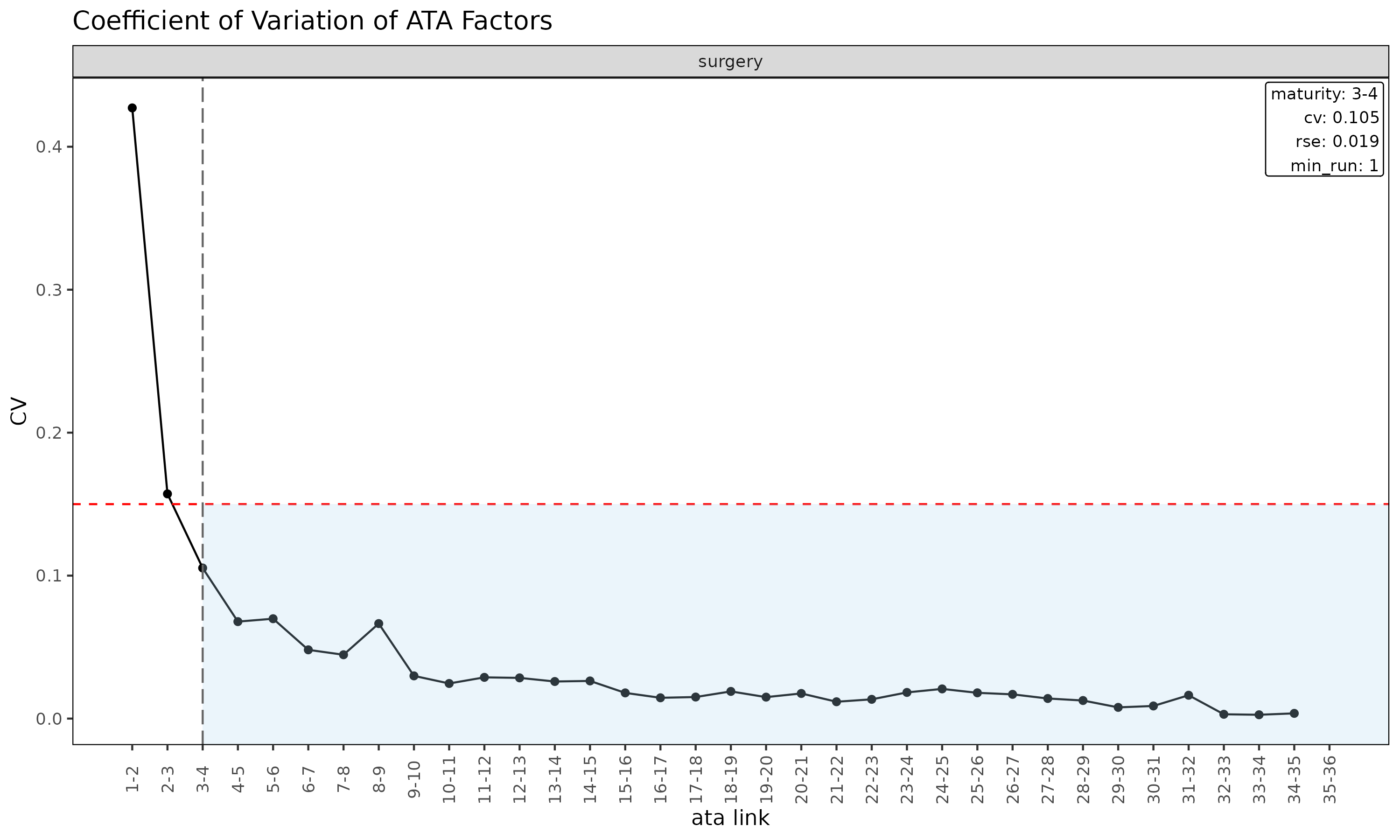

mat <- detect_maturity(

tri_sur,

loss = "loss",

max_cv = 0.15, # CV must be below this

max_rse = 0.05, # RSE must be below this

min_valid_ratio = 0.5, # at least 50% finite cohorts at the link

min_n_valid = 3L, # at least 3 finite cohorts

min_run = 1L # at least 1 consecutive mature link

)

print(mat)

#> Key: <coverage>

#> coverage ata_from change ata_link mean median wt cv

#> <char> <num> <num> <char> <num> <num> <num> <num>

#> 1: surgery 3 4 3-4 1.434507 1.400098 1.417706 0.1053282

#> f f_se rse sigma n_cohorts n_valid n_inf n_nan

#> <num> <num> <num> <num> <num> <num> <num> <num>

#> 1: 1.417706 0.02651852 0.01870522 1372.883 33 33 0 0

#> valid_ratio

#> <num>

#> 1: 1The result is a row per group with the first development link

satisfying all thresholds, carrying that link’s full statistics. The

threshold arguments are also stored as attributes on the returned

Maturity object.

Threshold semantics

-

max_cv— coefficient of variation of the observed ATA factors at the link. Caps relative spread regardless ofalpha. -

max_rse— relative standard error of the WLS-estimated factorf. Captures parameter uncertainty rather than residual spread. -

min_valid_ratio— minimum share of cohorts with a finite ATA at the link. Guards against links where most observations are zero / NA / Inf. -

min_n_valid— minimum count of finite cohorts at the link. An absolute floor for thin-data tails. -

min_run— minimum number of consecutive mature links. Withmin_run = 1L(default) the first qualifying link wins; setting it to2Lor higher requires sustained stability.

Tune these to the portfolio’s volatility profile. Tight thresholds

(e.g. max_cv = 0.05) push maturity later; loose thresholds

push it earlier. The link diagnostic plot makes the result easy to read

— each CV gets its own panel and a vertical line marks the maturity

point where CV first drops below max_cv:

Use in fitting

detect_maturity() is also called internally by

fit_ata(), fit_cl(), and

fit_ratio(method = "sa") via the maturity

argument. It accepts four forms:

-

NULL— no detection (worker default for standalone calls). - a pre-built

Maturityobject — fromdetect_maturity(), or frommaturity_at()for a manual override. -

"auto"— internaldetect_maturity()with defaults (the default forfit_ratio(method = "sa")andfit_loss()). - a function of one triangle returning a

Maturity— typicallymaturity_spec(), which forwards custom detection thresholds.

fit_ata(tri_sur, loss = "loss",

maturity = maturity_spec(max_cv = 0.08, min_run = 2L))

fit_ratio(tri_sur, method = "sa",

maturity = maturity_spec(max_cv = 0.08))For fit_ratio(method = "sa") the detected maturity point

determines the dev at which the projection switches from ED (early dev)

to CL (later dev).

Convergence detection

Maturity answers “from which development period are link factors reproducible across cohorts?”. That is necessary for chain-ladder projection but not sufficient for declaring a portfolio’s projected loss ratio converged. In long-duration health insurance both and arise mechanically as cumulative denominators grow — independent of whether the underlying experience has actually settled. A criterion built on those quantities passes automatically with , not because of true convergence (the inertia failure mode).

detect_convergence() detects the convergence

point

— the first dev

at which the projected portfolio loss ratio is observed to be

stable, in a sense the user picks via method =. It is the

natural counterpart to

:

-

(

detect_maturity()) marks where link factors become reproducible. - marks where the projection itself stops moving with new data.

Long-duration health portfolios may cross early yet remain far from .

The four stability methods

Convergence cannot be measured asymptotically from finite data, only

observed up to the maximum available dev dev_max

().

The detector runs a rolling backtest() over a sequence of

candidate dev points dev_cand

,

builds the projected ultimate LR path ratio at each one,

then evaluates four stability metrics on that path. The

method = argument selects which metric defines

conv_k; all four are returned for inspection regardless of

the choice.

| Method | Metric | Captures | Misses |

|---|---|---|---|

"window" |

range of ratio over the next window

valuations |

local stability (no zig-zag) | slow monotone drift below max_drift per window |

"tail" (default) |

range of ratio over [k, K_{\max}]

|

global stability up to dev_max; catches monotone

drift |

needs

tail points; first-pass is conservative (later than

"window") |

"slope" |

,

OLS slope of ratio ~ k on [k, K_{\max}]

|

systematic trend (signed direction) | oscillation that averages out to zero slope |

"all" |

intersection of "window" + "tail" +

"slope"

|

every shape above | (strictest) |

Across all methods a cross-cohort dispersion clause

dispersion[i] < max_dispersion is required in addition —

incremental loss ratios at that dev must agree across cohorts (computed

via the robust

metric). The constant

inside dispersion is the standard

MAD

correction, so

reads as a robust, outlier-resistant coefficient of variation of

incremental LR.

Why not an SE-normalised criterion? Earlier versions of this detector implemented from the original methodology paper (Section 11; the paper uses instead of , same axis). On large portfolios that form is structurally broken: shrinks as while has a numerical noise floor (~ LR units), so the ratio diverges and the criterion never fires — even on synthetic data that is visibly stable. The drift-based methods replace SE-normalisation with a data-size-independent threshold.

Notation

Standard chain-ladder convention:

indexes cohort (origin period),

indexes development period. detect_maturity() returns

,

detect_convergence() returns

— both live on the same

axis.

| Code | Math | Meaning |

|---|---|---|

dev_max |

Maximum observable dev (a scalar) | |

dev_cand |

Integer vector of candidate dev points | |

ratio[i] |

Portfolio LR projection at dev = dev_cand[i]

|

|

revision[i] |

Adjacent-step revision (diagnostic only) | |

drift_window[i] |

over | Local window range |

drift_tail[i] |

over | Tail range (global stability) |

slope[i] |

OLS slope on | |

dispersion[i] |

Robust cross-cohort spread of incremental LR | |

mat_k |

Maturity point (lower bound on candidates) | |

conv_k |

The detected convergence point |

Basic usage

res <- detect_convergence(tri_sur)

print(res)Mock output (no convergence detected on this run-off):

#> <Convergence>

#> method : tail

#> conv_k : NA

#> mat_k : 4

#> dev_max : 30

#> candidates : 25

#> passes :

#> window : 0/25 (drift_window < 0.01 & dispersion < 0.15)

#> tail : 0/25 (drift_tail < 0.01 & dispersion < 0.15) <- method

#> slope : 0/25 (|slope| < 0.001 & dispersion < 0.15)

#> all : 0/25 (window AND tail AND slope)The summary data.table has one row per candidate dev

with every metric and per-method pass flag:

#> dev ratio revision drift_window drift_tail slope dispersion

#> <int> <num> <num> <num> <num> <num> <num>

#> 1: 4 0.62 NA 0.07 0.07 0.001 0.47

#> 2: 5 0.63 0.01 0.06 0.06 0.001 0.47

#> ...

#> pass_window pass_tail pass_slope pass

#> <lgl> <lgl> <lgl> <lgl>

#> 1: FALSE FALSE FALSE FALSE

#> 2: FALSE FALSE FALSE FALSEThe Convergence object also reports the threshold

parameters (max_drift, max_slope,

max_dispersion, window,

holdout_max, min_n_cohorts) and metadata

attributes (groups, target,

dispatcher).

How it works: rolling holdout refits

For each dev_cand[i], the function backtests the LR

projection with holdout = dev_max - dev_cand[i] and

extracts the portfolio LR. Calls are cached per holdout depth so we

don’t redo work between adjacent candidates.

Example: with dev_max = 30, mat_k = 4,

holdout_max = 13 — candidates are

(25 in total), but only

with holdout = dev_max - k <= holdout_max get a finite

ratio[i]. The rest are masked to NA.

holdout_max defaults to

max(window, floor((dev_max - mat_k) / 2)). Raising it

widens the diagnostic window — at the cost of less data behind each

refit and hence noisier ratio near the lower edge.

Plot

plot(res)Five stacked panels share the dev axis:

-

ratio— the LR trajectory the metrics are computed from. -

drift_window— the local-window metric, with horizontal guide atmax_drift. -

drift_tail— the tail metric, same guide. -

|slope|— guide atmax_slope. -

dispersion— guide atmax_dispersion.

Vertical guides mark mat_k (dashed) and

conv_k (solid, only when non-NA). For each

metric panel, points below the red dashed line pass that clause. The

subtitle records the active method. This is also a quick

way to see which clause is binding: any panel that hovers above

its threshold blocks convergence under that method.

Threshold tuning

| Argument | Default | Meaning |

|---|---|---|

method |

"tail" |

Which stability metric defines conv_k. |

max_drift |

0.01 |

Drift cap on drift_window / drift_tail, in

LR units. Raise (e.g. 0.02–0.05) for noisier

or longer-tail books. |

max_slope |

1e-3 |

cap (LR per dev). |

max_dispersion |

0.15 |

Cross-cohort dispersion cap. |

window |

5L |

Drift window length

— number of consecutive valuations the "window" method

scans. Does not affect "tail" or

"slope". |

min_n_cohorts |

5L |

Below this cohort count, dispersion is

NA. |

Sweep max_drift to inspect sensitivity:

sapply(

c(0.005, 0.01, 0.02, 0.05),

function(d) detect_convergence(tri_sur, method = "tail", max_drift = d)$conv_k

)max_dispersion below

is difficult to attain in real portfolios because of single-period claim

noise; values above

usually indicate genuine cohort heterogeneity that warrants

detect_regime() before further modelling.

Reserving caveat

The detected conv_k is stability observed up

to dev_max, not an asymptotic guarantee.

Future development past dev_max is unknown. Treat

conv_k as a diagnostic for “from here on, what we observe

is stable”, not as proof that the projection will not drift later.

For reserving applications:

- Prefer

method = "tail"(default) or"all"over"window"."window"will declare convergence prematurely on slow monotone drifts that fit undermax_driftper window — exactly the silent-revision pattern that hurts reserves. - Always weigh the evidence span

dev_max - conv_k. Aconv_kneardev_max(say, span ) was confirmed by very few tail points; the same data might unconverge with one more diagonal. - Read the projected ultimate LR and its standard error from

fit_ratio()$summarydirectly.detect_convergence()is a diagnostic, not an estimator; the reserve point estimate and uncertainty come from the fit object.

Limitations

detect_convergence() is a thin layer over repeated

backtest() calls and inherits their constraints:

-

Identifiability:

conv_kcan be declared only whendev_max - mat_k >= window(or 2 for tail / slope). Short observation windows returnNAfor every method. -

Model conditioning: the projected LR is computed by

fit_ratio(), which internally composesfit_loss()(defaultmethod = "ed") andfit_premium(). Choices made inside that composition (loss method, regime filter, maturity argument) feed through toconv_k; passloss_method =,loss_regime =, etc. through...to override. -

Portfolio aggregation: the portfolio LR aggregates

per-group ultimates via premium weighting

(

sum(loss_ult) / sum(premium_ult)). Calendar-year shocks (regulatory changes, cost trend) can move every group together; the drift metrics will not separate that from genuine convergence. -

Multi-group triangles:

dispersionis currently collapsed across groups by median. When groups behave differently, running each group separately is recommended.

Regime detection

The two diagnostics above live on the development axis and assume the cohorts are homogeneous. When a portfolio undergoes a rate revision, coverage restructure, or underwriting overhaul, that assumption breaks: recent underwriting cohorts behave differently from earlier ones. Two questions follow:

- Are recent underwriting cohorts behaving differently from earlier cohorts?

- If so, when did the change happen?

In long-term insurance, cohort patterns most commonly break under one of four triggers:

- Drastic premium adjustment — large up- or down-revision of rates.

- Product coverage content change — restructuring of benefits, exclusions, or term.

- Sum insured limit change — adjustment of per-policy maximum.

- Underwriting guideline change — eligibility, declarations, or loading rule revisions.

A visual inspection of plot(tri_sur) can suggest that

recent cohorts have lower early loss ratios than older ones, but

eye-balling a bundle of trajectories is an unreliable way to locate a

structural shift — especially when observation windows differ across

cohorts.

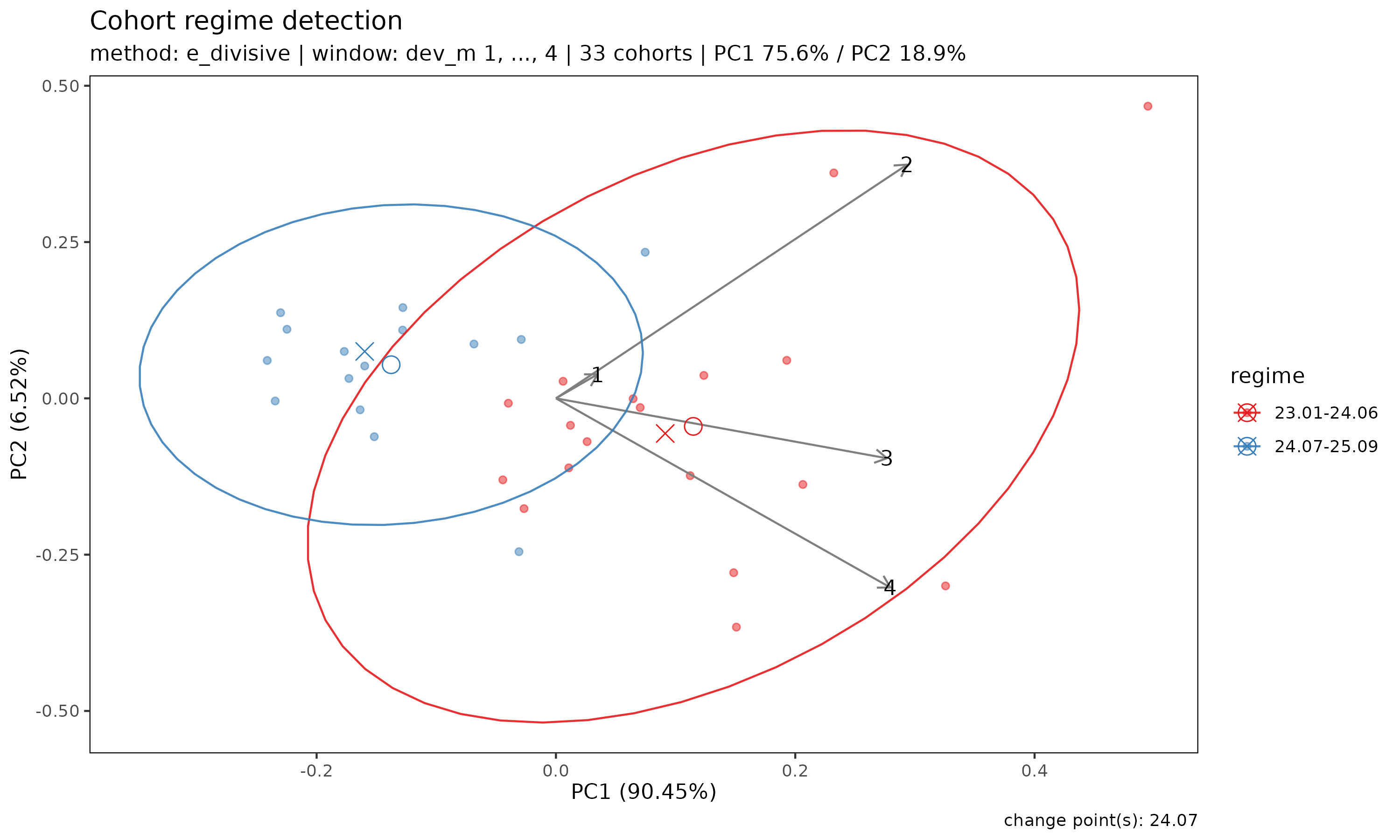

detect_regime() answers both questions in one call —

grouping underwriting cohorts into regimes (groups of

cohorts that share similar loss dynamics) and reporting the break dates

between groups. It treats each underwriting cohort as a feature vector

(its trajectory over the first window development periods),

orders cohorts by underwriting date, and applies a change-point or

clustering method to the resulting multivariate sequence.

r <- detect_regime(tri_sur, method = "e_divisive")

r

#> <Regime>

#> method : e_divisive

#> loss : ratio

#> treatment : segment_bridged

#> window (window) : dev_m 1-4

#> cohorts : 33 analysed (3 dropped)

#> regimes : 2

#> changes : 24.07

#> PC1 / PC2 : 75.6% / 18.9%The window argument controls how many development

periods define the cohort feature vector. Only cohorts observed for at

least window periods are analysed; cohorts with shorter

windows are dropped. Increasing window captures more of the

trajectory but drops more recent cohorts. With the default

window = "auto", a maturity-aware sweep picks the largest

window that retains enough cohorts.

Summary and per-regime membership

summary(r)

#> Cohort regime detection summary

#> method : e_divisive

#> loss : ratio

#> treatment : segment_bridged

#> window : dev_m 1-4

#> cohorts : 33 analysed (3 dropped)

#>

#> Regimes (2):

#> 1: 23.01-24.06 (18 cohorts)

#> 2: 24.07-25.09 (15 cohorts)

#>

#> Changes: 24.07

r$labels

#> coverage cohort regime regime_id

#> <char> <Date> <fctr> <int>

#> 1: surgery 2023-01-01 23.01-24.06 1

#> 2: surgery 2023-02-01 23.01-24.06 1

#> 3: surgery 2023-03-01 23.01-24.06 1

#> 4: surgery 2023-04-01 23.01-24.06 1

#> 5: surgery 2023-05-01 23.01-24.06 1

#> 6: surgery 2023-06-01 23.01-24.06 1

#> 7: surgery 2023-07-01 23.01-24.06 1

#> 8: surgery 2023-08-01 23.01-24.06 1

#> 9: surgery 2023-09-01 23.01-24.06 1

#> 10: surgery 2023-10-01 23.01-24.06 1

#> 11: surgery 2023-11-01 23.01-24.06 1

#> 12: surgery 2023-12-01 23.01-24.06 1

#> 13: surgery 2024-01-01 23.01-24.06 1

#> 14: surgery 2024-02-01 23.01-24.06 1

#> 15: surgery 2024-03-01 23.01-24.06 1

#> 16: surgery 2024-04-01 23.01-24.06 1

#> 17: surgery 2024-05-01 23.01-24.06 1

#> 18: surgery 2024-06-01 23.01-24.06 1

#> 19: surgery 2024-07-01 24.07-25.09 2

#> 20: surgery 2024-08-01 24.07-25.09 2

#> 21: surgery 2024-09-01 24.07-25.09 2

#> 22: surgery 2024-10-01 24.07-25.09 2

#> 23: surgery 2024-11-01 24.07-25.09 2

#> 24: surgery 2024-12-01 24.07-25.09 2

#> 25: surgery 2025-01-01 24.07-25.09 2

#> 26: surgery 2025-02-01 24.07-25.09 2

#> 27: surgery 2025-03-01 24.07-25.09 2

#> 28: surgery 2025-04-01 24.07-25.09 2

#> 29: surgery 2025-05-01 24.07-25.09 2

#> 30: surgery 2025-06-01 24.07-25.09 2

#> 31: surgery 2025-07-01 24.07-25.09 2

#> 32: surgery 2025-08-01 24.07-25.09 2

#> 33: surgery 2025-09-01 24.07-25.09 2

#> coverage cohort regime regime_id

#> <char> <Date> <fctr> <int>Visualisation

plot(r) produces a PCA scatter of cohort trajectories

coloured by detected regime. If the regimes are well-separated in PCA

space, the structural shift is visually confirmed:

plot(r)

Arrows indicate the loadings of each development-period feature on the PC axes — useful for reading how the regimes differ (e.g. whether the shift primarily affects early or late development).

Choice of loss

The loss argument controls which signal the

change-point algorithm operates on. Different metrics surface different

kinds of regime change, and each has its own failure mode. Pick the

metric that matches the event you suspect — and always cross-check with

domain knowledge. The order

c("ratio", "loss_ata", "premium_ata", "loss_ed", "premium_ed", "loss", "premium")

runs from cleanest to riskiest.

| Scenario to detect | Recommended loss

|

Caveat |

|---|---|---|

| General LR projection accuracy (default) | "ratio" |

Differential growth (loss vs premium scaling unevenly) can produce smooth drift mis-labelled as a sharp break. |

Loss development speed change (CL f) |

"loss_ata" (diagnostic)

|

Loses dev = 1 row + complete-row requirement -> sample size shrinks; over-sensitive on low-CV factors. |

| Premium recognition speed change |

"premium_ata" (diagnostic)

|

Same caveats as "loss_ata". |

Loss intensity per unit premium (ED g) |

"loss_ed" (diagnostic)

|

Cross-normalised by premium; harder to interpret in isolation. |

Same as premium_ata (API symmetry) |

"premium_ed" (alias)

|

Equivalent to premium_ata after PCA

standardization. |

| Loss level shift (claim handling, coverage) | "loss" |

Raw cumulative — book-size growth dominates; false positives common. |

| Premium level shift (rate, channel) | "premium" |

Same caveat as "loss". |

Notes:

-

"ratio"is the default because the loss ratio is the package’s projection metric and is naturally scale-invariant (immune to book-size growth). -

"loss"/"premium"use the raw cumulative columns and are most useful when the suspected event is a sudden absolute level shift (e.g. a channel termination dropping premium volume). Smooth book growth will frequently produce false positives — read every result alongside a known timeline of underwriting / claims-handling events. -

"loss_ata","premium_ata","loss_ed"are diagnostic metrics derived inline (not stored on theTriangle). They map directly to the CLf-factor / EDg-factor used during fitting, so a change detected here corresponds to a violation of the model’s stationarity assumption. Use them to attribute a regime change to a specific structural mechanism.

# Try several metrics and compare the changes they surface

detect_regime(tri_sur, loss = "ratio")

detect_regime(tri_sur, loss = "loss")

detect_regime(tri_sur, loss = "loss_ata")The changes across metrics are usually similar for strong, real regime shifts and diverge when the signal is weak or driven by book-size growth — both useful diagnostics.

Choice of method

-

"e_divisive"— preferred default. Multivariate, non-parametric, auto-detects the number of regimes at a given significance level, so it requires no a priori choice ofn_regimes. -

"hclust"— Ward hierarchical clustering on the scaled feature matrix, cut ton_regimesclusters (default2). Ignores chronological order and is best used as a sanity check: if the chronological method locates a change at timetandhclustproduces the same two groups (all pre-tin one cluster, all post-tin the other), the shift is structural rather than an artefact of the method.

In practice, agreement across both methods — as in the surgery

example above, where "e_divisive" and "hclust"

both locate 24.04 as the regime boundary — is strong

evidence of a real underwriting / rate shift.

Forcing the number of regimes

To compare a fixed number of regimes — for example, two-vs-three

regime hypotheses — pass n_regimes:

r2 <- detect_regime(tri_sur, method = "e_divisive", n_regimes = 3)

summary(r2)

#> Cohort regime detection summary

#> method : e_divisive

#> loss : ratio

#> treatment : segment_bridged

#> window : dev_m 1-4

#> cohorts : 33 analysed (3 dropped)

#>

#> Regimes (3):

#> 1: 23.01-24.06 (18 cohorts)

#> 2: 24.07-25.06 (12 cohorts)

#> 3: 25.07-25.09 (3 cohorts)

#>

#> Changes: 24.07, 25.07For "e_divisive", n_regimes is a request

(the algorithm will return up to that many regimes if supported by the

data). For "hclust", it is a hard cut.

Multi-group detection

A Triangle built with multiple groups can be passed

directly — detection runs independently per group and results are

gathered into a single Regime object.

tri_all <- as_triangle(

experience,

groups = "coverage",

cohort = "uy_m",

calendar = "cy_m",

loss = "incr_loss",

premium = "incr_premium"

)

r_all <- detect_regime(tri_all, by = "coverage", method = "e_divisive")

r_all$changes

#> coverage change regime_id pre_value post_value magnitude

#> <char> <Date> <int> <num> <num> <num>

#> 1: surgery 2024-07-01 2 0.9065895 0.5479919 0.3585976In multi-group mode r_all$changes is a

data.table with the group column plus a change

Date column; r_all$labels likewise gains the group column;

r_all$n_regimes is a named integer vector keyed by group

value. The r_all$multi_group flag distinguishes the layout

from the single-group scalar form. If a group has too few cohorts for

the chosen window, that group is skipped with a warning

(others continue). If all groups fail,

detect_regime() errors out. plot(r_all)

returns a named list of per-group ggplot panels.

Regime filtering of fits

detect_regime() is a preprocessing diagnostic,

not a modification of the fit_ratio() framework. Its output

is used in two ways:

-

Stratified fitting: if two clearly distinct regimes

are detected, fitting

fit_ratio()separately on each regime subset often yields sharper convergence-region LR estimates than a pooled fit. -

In-fit filtering: a

Regimecan be passed straight into thefit_*family as a data filter, dropping pre-change cohorts from factor estimation. The rest of this section covers that path.

Why a hybrid filter

When chain ladder is fitted on the full triangle after a regime

change, old-cohort link factors leak into the new-cohort projections,

which shows up as a monotone drift across diag_summary in

backtest(). The recent = N argument suppresses

some of this drift, but a calendar-diagonal cut is symmetric across both

axes — it discards older cohorts’ young-dev cells too, where the ED

region was already stable. The natural fix is asymmetric:

- Pre-maturity (ED region): horizontal cut — keep only post-change cohorts.

-

Post-maturity (CL region): diagonal cut — keep only

the recent

Ncalendar diagonals.

loss_regime (and its premium-side sibling

premium_regime) implements that split.

Two-axis asymmetry

| Axis | Number of changes | Source |

|---|---|---|

| x (maturity, ED -> CL) | exactly one per group | fit_ata$maturity |

| y (regime change) | zero or many per group | detect_regime$changes |

The maturity point

is a single internal switch produced by detect_maturity().

Regime changes are exogenous events — there can be none, one, or

several. When a Regime object carries multiple changes, the

treatment slot decides how downstream fits use them:

Both treatments mask the triangle to a bridged development

band: each segment’s natural mini-triangle wall

(dev >= max_cal - seg_last + 1) is widened by a

calendar-diagonal bridge anchored at the next (newer) segment’s

first-cohort midpoint dev. The bridge closes the factor gaps that would

otherwise open at the segment boundaries, so the band carries a

continuous run of age-to-age factors and every cohort projects

to the full development length – including the newest cohorts,

which the pre-regime cells of older cohorts would never reach on their

own.

-

treatment = "segment_bridged"(default): pool the whole bridged band into a single factor estimate. Every cohort at devkuses the samef_k, drawn from whichever (most recent) cohorts reach that dev inside the band. The development pattern is treated as shared across regimes; only the band’s lower boundary is regime-aware. -

treatment = "segment_bridged_borrowed": estimate factors per segment (early-development factors stay regime-specific), then borrow the late-development factors a segment cannot reach from another segment that can. Use this when the early development pattern genuinely differs across regimes but the long-tail development is shared.

Pick the treatment when constructing the Regime:

# Pooled bridged band (default)

regime_at(change = c("2022-01-01", "2024-04-01"))

# Per-segment factors with late-dev borrowing

regime_at(change = c("2022-01-01", "2024-04-01"),

treatment = "segment_bridged_borrowed")

detect_regime(tri_sur, treatment = "segment_bridged_borrowed")API

fit_ratio() takes two role-specific regime arguments —

loss_regime (loss-side filter) and

premium_regime (premium-side filter; defaults to

loss_regime). fit_loss() /

fit_premium() take a single regime argument.

backtest() mirrors fit_ratio with

loss_regime / premium_regime. The workers

(fit_ata, fit_ed, fit_cl,

fit_intensity) expose the same single regime

argument. All accept the same four input types:

| Input | Behaviour |

|---|---|

NULL (default) |

no filtering — backwards compatible |

Regime object |

output of detect_regime() or

regime_at()

|

"auto" sentinel |

calls detect_regime() internally on the triangle |

function(tri) -> Regime |

closure that returns a Regime from a triangle |

Raw Date / character / vector input is no longer

accepted — wrap it in regime_at() first to make the change

explicit:

# Manual change date via regime_at() — wrap a literal date in a Regime

fit_ratio(tri_sur, method = "sa", recent = 18L,

loss_regime = regime_at(change = "2024-07-01"))

# Regime object from detect_regime() directly

reg <- detect_regime(tri_sur)

fit_ratio(tri_sur, method = "sa", recent = 18L, loss_regime = reg)

# "auto" sentinel — detect_regime() is run internally

fit_ratio(tri_sur, method = "sa", recent = 18L, loss_regime = "auto")

# Closure — defers detection until the fit sees the (filtered) triangle

fit_ratio(tri_sur, method = "sa", recent = 18L,

loss_regime = function(tri) detect_regime(tri))In simple modes (fit_ratio(method in

{"ed","cl"}) the same argument acts as a plain cohort

cut.

SA-mode hybrid behaviour

The hybrid split activates only for

fit_ratio(method = "sa") with both loss_regime

and recent:

- dev — ED region: post-change cohorts only.

- dev

— CL region: latest

recentdiagonals only (full triangle ifrecent = NULL).

The maturity point itself is found in a two-pass procedure: first on the raw triangle (so noisy post-change windows do not destabilise ), then the hybrid filter is applied to the actual fit using the fixed .

plot_triangle(view = "usage") visualises which cells

each filter configuration feeds to fit_ratio:

plot_triangle(tri_sur, view = "usage", holdout = 6L) # full

plot_triangle(tri_sur, view = "usage", recent = 12L, holdout = 6L) # recent

plot_triangle(tri_sur, view = "usage", regime = "2024-07-01", holdout = 6L) # change

plot_triangle(tri_sur, view = "usage", recent = 12L,

regime = "2024-07-01", holdout = 6L) # hybridThe hybrid panel shows the dev-axis split that SA mode applies: a cohort cut on the ED side and a calendar diagonal cut on the CL side, joined at .

Case study — surgery cohort

The bundled experience dataset embeds a synthetic

2024-04 regime change in the surgery coverage. Backtests on the same

triangle with four variants:

reg <- detect_regime(tri_sur)

bt_full <- backtest(tri_sur, holdout = 6L)

bt_recent <- backtest(tri_sur, holdout = 6L, recent = 18L)

bt_change <- backtest(tri_sur, holdout = 6L, loss_regime = reg)

bt_hybrid <- backtest(tri_sur, holdout = 6L, recent = 18L,

loss_regime = reg)Reproduced from dev/regime_backtest_hybrid.R:

| Variant | drift (cal30 - cal25) | overall mean |

|---|---|---|

| full | +4.50pp | -1.25% |

| recent = 18 | +2.03pp | -3.45% |

| loss_regime + recent = 18 | -0.69pp | +0.03% |

Two columns summarise the A/E Error = actual / proj - 1

(positive = under-projection) measured on the held-out diagonals:

- drift (cal30 - cal25): A/E Error aggregated by calendar diagonal, then the (latest - earliest) difference. Captures whether the prediction error is monotonically changing across the hold-out window — the signature of a regime change the static model has not absorbed.

- overall mean: cell-level mean A/E Error across all held-out cells — the model’s directional bias.

Drift collapses from +4.50pp under full to -0.69pp under

the hybrid filter; the overall mean returns to ~0.

Multi-group handling

detect_regime() assumes a single-group triangle for

in-fit filtering. For a portfolio with multiple coverage

groups, call it per group:

fits <- lapply(unique(experience$coverage), function(g) {

tri_g <- as_triangle(

experience[coverage == g],

groups = "coverage",

cohort = "uy_m",

calendar = "cy_m",

loss = "incr_loss",

premium = "incr_premium"

)

reg_g <- detect_regime(tri_g)

fit_ratio(tri_g, method = "sa", recent = 18L, loss_regime = reg_g)

})A future extension may accept

loss_regime = list(surgery = regime_at(...), cancer = regime_at(...)).

Today only NULL / Regime / "auto"

/ closure are supported.

Filtering limitations

If the post-change window is too short (small n_post),

the ED intensity

and link factors

become noisy. A practical threshold is n_post

.

Below that, prefer recent alone, or wait for

credibility-weighted blending of pre- and post-change factors

(planned).

Note also that loss_regime / premium_regime

only filter the data feeding link factor estimation. Once the factors

are fixed, all cohorts share them, so pre-change ultimates inherit the

post-change dynamics.

A defensible workflow

The three diagnostics separate cohort homogeneity, link reproducibility, and level convergence — properties that coincide in P&C run-off but must be verified independently in long-duration health insurance:

- Run

detect_regime(). If multiple regimes exist, fit each group separately, or passloss_regime =/regime =into the fit / backtest call. - For each homogeneous group, compute

via

detect_maturity(). - Run

detect_convergence()to obtain . Read the projected ultimate loss ratio fromfit_ratio()$summaryand apply the reserving caveat.

See also

-

?detect_maturity,?detect_convergence,?detect_regime,?regime_at,?maturity_spec,?fit_ratio,?backtest. -

vignette("backtest")— the rolling holdout machinery thatdetect_convergence()and the regime filter case study are built on. -

vignette("projection")—fit_ratio()and the"sa","ed","cl"methods.